The Grandparent's Guide to Teaching a Grandchild About Money

From Annaline Dinkelmann, former Morgan Stanley professional. What to give, what to say, and how to turn a financial gift into a story your grandchild will tell.

What I Have Learned From the Grandparents I Work With

"Grandparents are the most powerful financial teachers most children ever have. Not because they have more money. Because they have more time, more story, and more permission."

— Annaline Dinkelmann, Junior Wall Street

What to Give: The Four Options

Grandchild gift for birthdays, graduation, a religious holidays or just because. The question is not "which is best". The question is "which one becomes a conversation."

1

Cash or a Gift Card

The most common. The least remembered. Easy to give, easy to spend, and nearly impossible to turn into a lasting lesson.

2

A Savings Bond

Familiar to your generation. Mostly invisible to the child. The interest rate is low. The story is boring. Better than nothing - but only just.

3

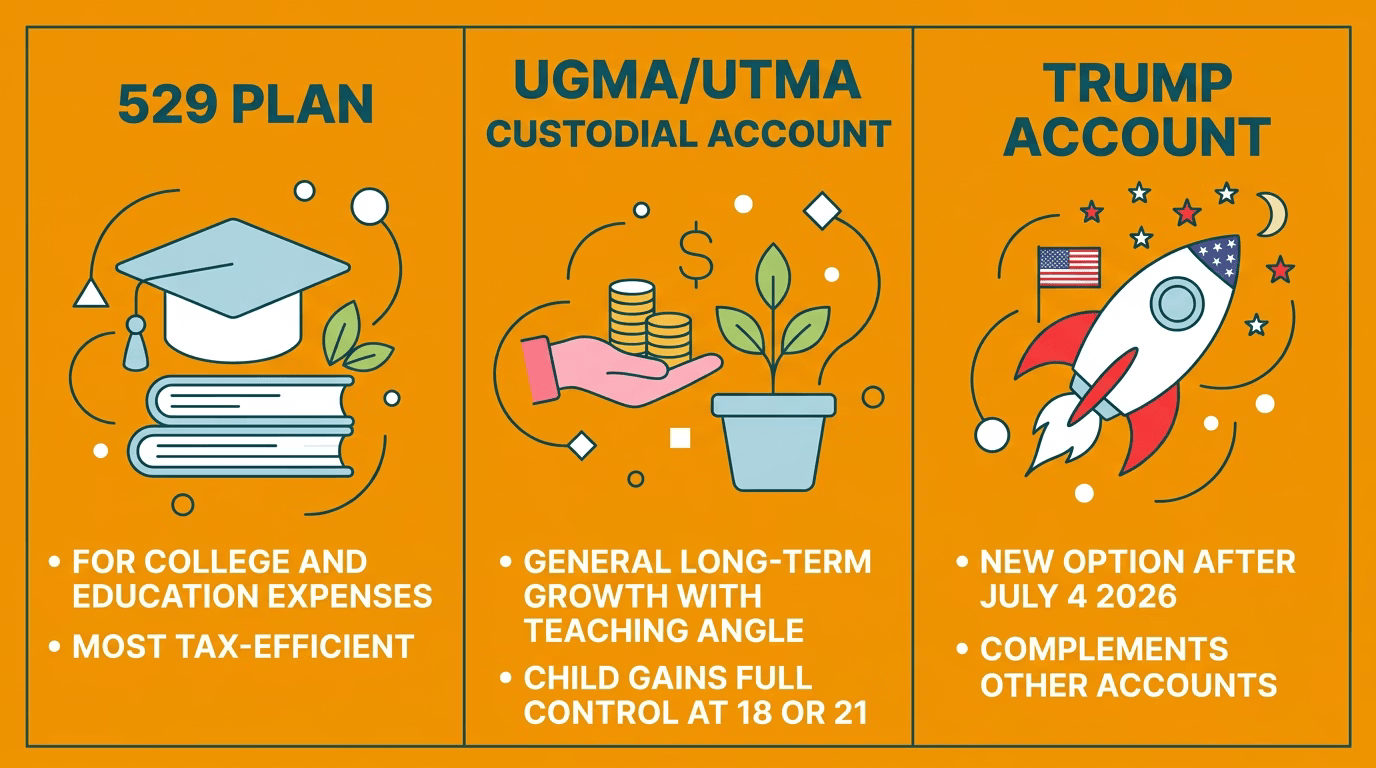

A 529 Plan Contribution

Tax-advantaged. Designed for college. Excellent vehicle if your grandchild is heading to a four-year program. Less flexible if they aren't.

4

A Custodial Brokerage Account

A UGMA or UTMA account in the child's name. Give them shares of Disney, Apple, or Nike. The account belongs to them at eighteen or twenty-one. The shares tell a story.

What to Say: A Script for the Conversation

The gift is half of the work. The other half is what you say when you give it. I have watched a $25 share of stock teach a child more than a $500 college fund contribution - because the $25 share came with a sentence the child remembered. The college fund contribution came with a tax form.

One of my students told me in a class "My grandpa gave me $500 and he told me that we can split the profit that I make."

That child was in my class and so eager to learn. He wanted to show his grandpa he could make money and he looked forward to his share of the profit.

What I learned from his story

→ Puts the gift inside a story, shared goal, something fun

→ Explains the mechanism without lecturing about it

→ Committed both of you to a yearly ritual - the conversation, not the money

→ Tells the child the relationship is bigger than the present

ⓘ

If your grandchild is under five, replace the share of stock with a picture book about money and a five-dollar bill in a glass jar where they can watch the pile grow. The principle is the same. The instrument is age-appropriate.

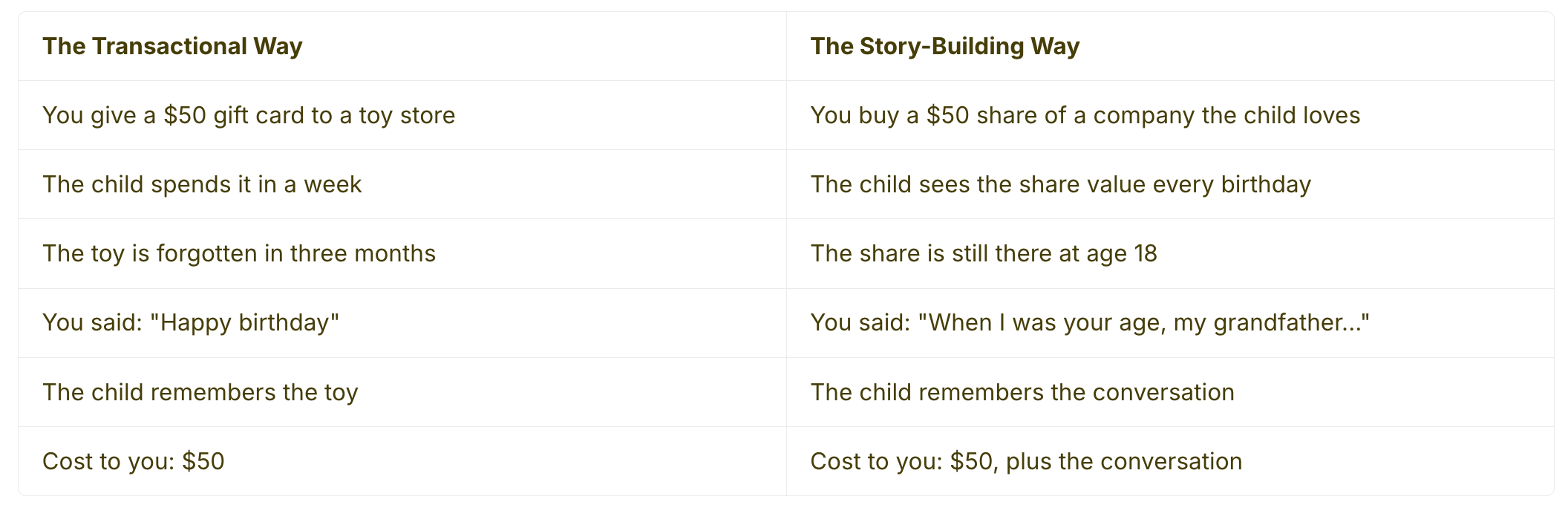

A $50 Gift, Two Very Different Outcomes

The money is the same. The outcome is not.

ⓘ

The most powerful financial gift a grandparent can give costs nothing extra — it's the story wrapped around the money.

When to Open a Custodial Account for a Grandchild

Rule 1: When the Gift Becomes Regular

If you are giving once and never again, a one-time gift card is fine. If you intend to give every birthday and every holiday for the next fifteen years, the account compounds the gifts in a way the gift card cannot.

Rule 2: In Coordination With the Parent

The parent will eventually need to talk to the child about this account. They cannot do that if they did not know it existed. Tell them what you are doing and why.

Rule 3: Match the Vehicle to Your Goal

Choose the account that fits your intention — not just the one you've heard of most.

The mechanics of opening an account take fifteen minutes online. The mechanics of choosing the right one take a conversation with someone who knows your family.

How the Junior Wall Street Workbook Series Becomes a Grandparent Gift

The Pattern That Works

The workbook series is built for parent-and-child use. But many of the families I work with use it as a grandparent-and-grandchild ritual instead.

Children remember rituals more than gifts. A workbook that gets opened together for ten years becomes the longest conversation about money the child ever has. That is a different scale than a toy.

ⓘ

If you want to give one workbook this year, start with Workbook 1 — the introduction. If you want to commit to the long version, buy the set. The full series is available on Amazon under Annaline Dinkelmann's author page.

Frequently Asked Questions

These are the questions grandparents ask most — about accounts, amounts, and how to actually start the conversation.

What is the best financial gift for a grandchild?

The best financial gift is one that comes with a conversation. A $25 share of a specific company the child knows, given with a story about why that company matters to you, will teach more than a $500 anonymous deposit into a college fund. The vehicle matters less than the ritual you build around it.

Can grandparents open a custodial account for a grandchild?

Yes. Any adult can open a UGMA or UTMA custodial brokerage account on behalf of a minor, regardless of relationship. The account is in the child's name; the grandparent is the custodian until the child reaches the age of majority - eighteen or twenty-one, depending on the state. You can also contribute to a 529 plan or a Trump Account opened by the parent.

How much can a grandparent give a grandchild tax-free?

In 2026, the annual gift-tax exclusion is $19,000 per person per recipient. Married grandparents can gift $38,000 per grandchild per year without filing gift-tax paperwork. Direct payments for education or medical expenses, made directly to the institution, do not count toward this limit at all.

More Answers: Choosing the Right Account and Starting the Conversation

Should grandparents give a 529 plan contribution or a UGMA?

A 529 plan is for college and similar qualified education expenses. A UGMA gives the child full flexibility at eighteen or twenty-one, which can be a feature or a bug depending on the child. If the grandchild is college-bound, the 529 is more tax-efficient. If you want the gift to teach investing along the way, a UGMA invested in a single recognizable company tells a better story.

How do I teach my grandchild about money?

Start with a story, not a lecture. Pick a gift that has a longer life than its dollar value — a share of stock, a workbook, a glass jar that fills up. Make the gift a yearly ritual: same time, same conversation, watch the number change. Children remember rituals more than amounts.

$238B

Given Annually

Grandparents collectively give $238 billion to grandchildren each year — most of it forgotten within months.

$25

Can Change Everything

A single $25 share of stock, given with a story, can teach more than a $500 anonymous college fund deposit.

$19K

Annual Tax-Free Limit

The 2026 gift-tax exclusion per grandchild. Married grandparents can give $38,000 per grandchild with no paperwork.

✓⃝

Ready to become a financial mentor, not just a gift-giver? Start with one share of a company your grandchild loves — and one sentence about why it matters to you.